David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companiesGetlink SE(EPA:GET) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

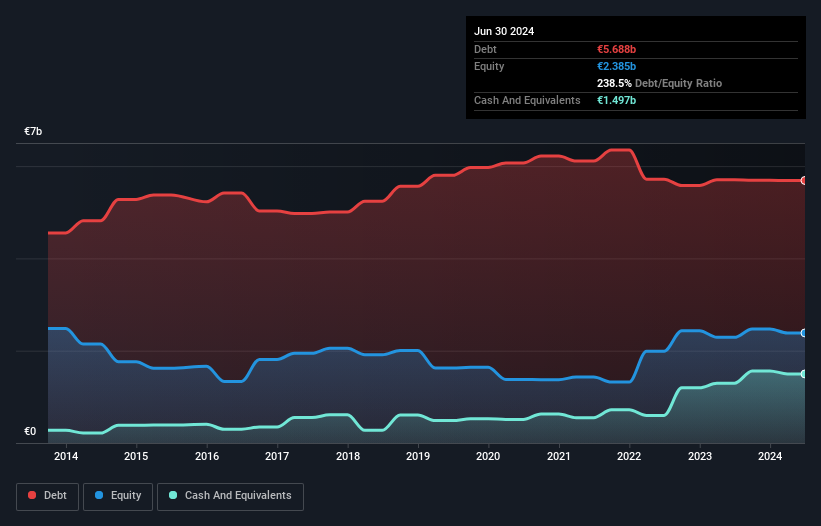

As you can see below, Getlink had €5.69b of debt, at June 2024, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has €1.50b in cash leading to net debt of about €4.19b

ENXTPA:GET Debt to Equity History August 14th 2024

How Healthy Is Getlink's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Getlink had liabilities of €583.0m due within 12 months and liabilities of €6.06b due beyond that. On the other hand, it had cash of €1.50b and €247.0m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by €4.90b.

This deficit isn't so bad because Getlink is worth €8.68b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Getlink has a debt to EBITDA ratio of 4.7 and its EBIT covered its interest expense 4.9 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Shareholders should be aware that Getlink's EBIT was down 20% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Getlink can strengthen its balance sheet over time. So if you're focused on the future you can check out this freereport showing analyst profit forecasts.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

As you can see below, Getlink had €5.69b of debt, at June 2024, which is about the same as the year before. You can click the chart for greater detail. On the flip side, it has €1.50b in cash leading to net debt of about €4.19b.

Our View

Getlink's EBIT growth rate and net debt to EBITDA definitely weigh on it, in our esteem. But its conversion of EBIT to free cash flow tells a very different story, and suggests some resilience. We should also note that Infrastructure industry companies like Getlink commonly do use debt without problems. When we consider all the factors discussed, it seems to us that Getlink is taking some risks with its use of debt. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 3 warning signs for Getlink (of which 2 are potentially serious!) you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt100% free, right now.

Using Too Much Debt?){kind=link}

0 Comments